SaaS 🏴☠️ | Property Management Fanatic 💙 | I write a bi-weekly newsletter to 4k PMs talking people, process and profit.

The State of Venture Capital In Property Management

I paused hitting send today.

But I have to get this off my chest.

I’ve had 30+ conversations with operators about whether they should sell their business.

In almost every conversation - people fall into four buckets:

- Seller motivated by personal situation (health, retirement, divorce)

- Seller trying to offload a distressed business (few admit this)

- Seller motivated by a cash payday that lines up with their long term goals

- Seller motivated by joining a bigger ship

#1 is purely personal.

#2 merits a conversation to see just how bad things are and assess if a rehab makes sense or not. 50/50.

#3 is exciting when the deal makes sense.

#4 is the most controversial and what I'm addressing in this newsletter.

The most critical aspect of joining a bigger ship… is inspecting the ship.

Not getting inspected… but doing the inspecting.

I’m talking about due diligence.

And THAT is the thing I see consistently neglected.

Far to often when I probe about the entity someone’s thinking about investing their life’s work into I get soft answers. “I don’t know, I never thought about that, can I even ask that?”

When I see friends cashing in for a monster payday in cash… I celebrate with them.

When friends sell their life's work for stock certificates… I’m anxious for them.

Of course, a subset of these bets will work out.

And that brings me to my first point.

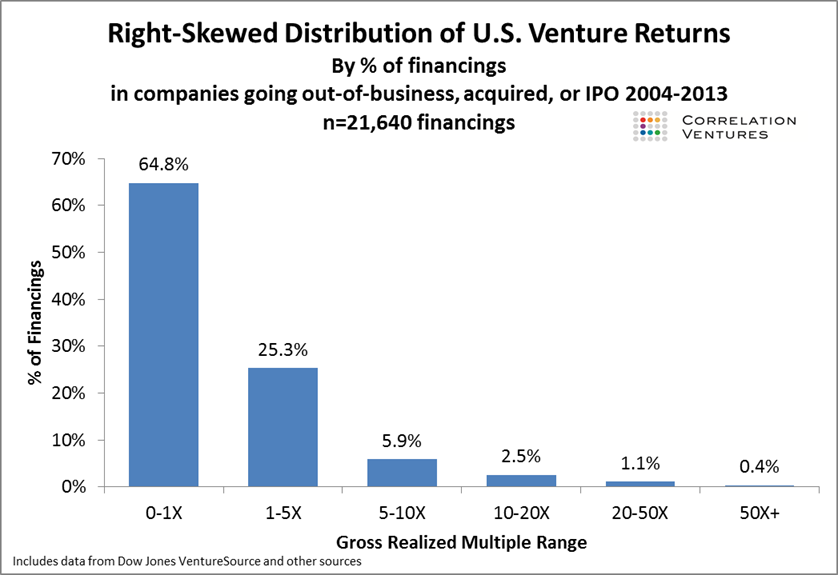

You need to understand the distribution curve you are dealing with.

What is the risk profile of the asset you are leaving versus entering?

Are you ok going from a slower-growing sure bet to a 1/XX chance at a big outcome?

Folks… this is NOT something I moralize about.

I. Like. Risk. Period.

More specifically, I like informed, calculated risk.

I don’t buy scratch-offs, invest in penny stocks, or fantasize about my beanie baby collection coming back around for a big payday.

I do, however, dig launching new products and companies and playing the odds.

What’s the difference?

I know nothing about the former and a fair bit about the latter.

Which brings me to my second point.

You have to truly understand the investment thesis.

Your analysis could involve complexity, or not, what matters is that you can explain in layman's terms how you are going to get your money back.

There can be no “we’ll figure out that part later” for major sections of the thesis.

For example… would you buy a small business for 10x revenue?

Would you invest in buying a large property management company for 10x revenue?

How about a really profitable, large, and growing PMC for 10x revenue?

Well... how long until you get your money back?

If we assume that company is insanely profitable… at scale (unprecedented) - then best case scenario we’re talking a 50% margin (insane) - which means it takes 20 years at a 10x multiple just to get your money back.

No sane investor dives in thinking it will take 20 years to see break even.

So what else are they betting on?

Let’s bake in a growth assumption and assume not only profitability at scale - but also being profitable while growing fast (half-unicorn/half-liger).

So maybe we collapse the payback timeline in half and now I am waiting 10 years to get paid back.

Still not that interesting.

BUT... then there's X.

X is the secret weapon.

X turns this from insanity to brilliance.

X involves unprecedented, game changing innovation.

Unfortunately, too often X is one the thing you're not qualified to evaluate or fully understand.

Which brings me to my final point.

NEVER IGNORE CASHFLOW

In your own business - always pay attention to cash flow.

When inspecting a potential acquirer - pay even closer attention to cash flow.

If the person wanting to buy you has none - you should be healthily afraid.

Why? Because there are only two ways to keep a biz without cash flow from going under.

- Raise Debt/Equity

- Become Profitable

That’s it - those are the options.

The problem is that companies that have done the former are rarely able to do the latter until they're so successful that they've basically already won.

Which means when you’re acquired by a funded company, everything - and I mean everything - is tied to their ability to raise more funding.

And in some cases, this works out.

Statistically the distribution pattern looks like this.

|

Do I root for every single founder looking to defy the odds?

Emphatically YES.

The difference is founders know they are taking a low probability, high upside bet.

But I don’t hear that same tone coming through from operators looking to sell.

I hear a lot about the potential upside and very little about the dramatically more likely downside.

And that feels off to me.

Folks, I don’t have a crystal ball.

I don’t know how it’s all going to break.

But where I have an extreme amount of conviction.

Is in the idea of going in wide-eyed fully assessing the risk.

Because a risk-adjusted return is the gold standard in the game of investment returns.

If you don’t really understand the risk - you shouldn’t expect returns.

In summary:

- You are the world's foremost expert on your business

- Never defer to people you think are smarter than you - the less you understand the deeper you need to press.

- Groupthink should make you think more, not less

- Don't take any wooden nickels

- Value always comes back to cashflow. Period.

Thank you for reading.

I’d love to hear what part of the podcast stuck out to you.

- JAAM

P.S. - Today's renters do not want to talk with you in person.

P.P.S. - Letter to employees from AppFolio CEO, Shane Trigg, explaining 9% layoff. Shane is a strong leader guiding the org toward profitability, they will bounce back.

P.P.P.S. - Investment outlook in private equity markets from Forge Global

P.P.P.P.S. - Agency is everything < This is a life message from me to the 🌎

P.P.P.P.P.S - Failure to face the truth < Love this founder and his POV.

Quote

Visual

---

Know someone that would enjoy the newsletter? They can subscribe here.

Jordan Muela

SaaS 🏴☠️ | Property Management Fanatic 💙 | I write a bi-weekly newsletter to 4k PMs talking people, process and profit.

There was a moment where our industry was star struck by the outside capital pouring in to fund VC-Backed property management companies. Now those companies are going under one by one. Yesterday the most well funded player in the category announced it was acquired by RoofStock. Mynd raised over $200M at close to a billion dollar valuation. Their thesis was pure play tech augmented by people: Mynd’s tech product is complemented by “boots on the ground” people in local markets, improving the...

After 7 years I've exited ProfitCoach. Watch the full story. Why did I exit? One word: Focus. Long term concentrated focus on a singular goal at the exclusion of all else. In practice this looks like saying no to fantastic opportunities I both believe in AND want to do. If it's not excruciating to say no to - you're not really focused. "The difference between successful people and really successful people is that really successful people say no to almost everything." – Warren Buffett. Not...

Note: Ready to build your 2024 growth strategy? Come to the All Bound conference this December in Austin, TX. --- Early in my career I viewed neutrality as weakness. The term “fence sitter” comes to mind. Make up your mind… pick a side. I felt safe and strong knowing what team I was on. Fast forward to today and my leadership style looks very different. Why? Because scaling has taught me one thing above all. Neutrality is critical to effective leadership. Neutral means open. Maximally...